Difference between Balance Sheet Account and Profit & Loss Account

Difference between Balance Sheet Account and Profit & Loss Account

In SAP FI a G/L[general ledger] account is needed to record business transactions and financial reports are generated based on the transactions booked against the G/L accounts. In SAP FI there are two types of G/L accounts: 1. Balance Sheet Account 2. P&L (profit & Loss) statement account.

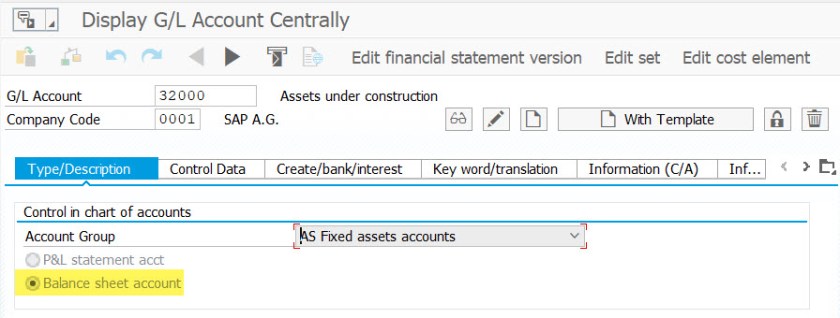

Balance Sheet Account: It is a financial statement which summarizes a company’s assets, liabilities and equity for a specific time period.

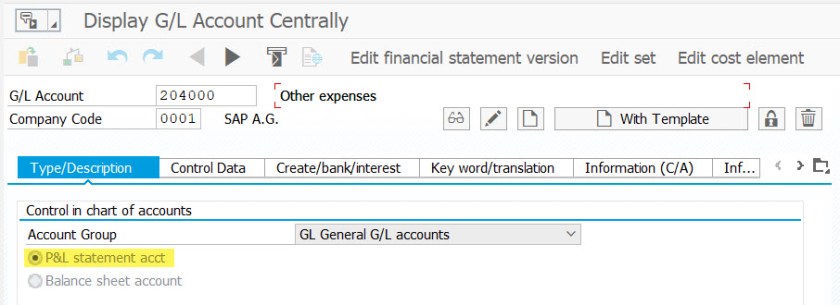

Profit & Loss Statement Account: It is a financial statement which summarizes costs, expenses and revenues incurred for a specific time period. Expenses/Losses goes to the debit side where as profit/income goes to credit side.

Differences:

1.

- Balance sheet accounts are prepared at the end of the financial year and talks about company’s assets, liabilities and capital.

- Profit & Loss statement accounts show income, expenses, gains and losses of a company during a period of time. At the end of financial year, net profit or net loss will be moved to the capital account of the balance sheet statement.

2.

- Balance sheet accounts balances is carried forward to the next financial year.

- Profit & Loss accounts balance is moved to the retained earning account.

3.

- Balance sheet accounts are not defined as cost elements.

- Profit & Loss accounts have to be defined as cost elements.

4.

- Balance sheet accounts can be defined with open item management indicator to perform clearing.

- Profit & Loss accounts won’t be defined with open item management indicator.

5.

- Reconciliation account types can be maintained for balance sheet accounts to create asset, customer , vendor and contract accounts receivables.

- Profit & Loss accounts can’t be defined as reconciliation accounts.